First steps after someone dies: is there a Will?

Last updated: July 2026 — England & Wales

When someone dies, it can be difficult to know what needs to happen first. Families often feel pressure to act quickly, but the first priority is usually not to distribute possessions, close everything down, or start making promises.

The first priority is to get organised, protect the estate, and work out whether there is a valid Will.

This guide is for family members, executors and would-be administrators in England and Wales. It helps you identify the immediate steps, avoid common mistakes, and work out which route may apply next.

It is general information only. It is not a full probate guide or personal legal advice.

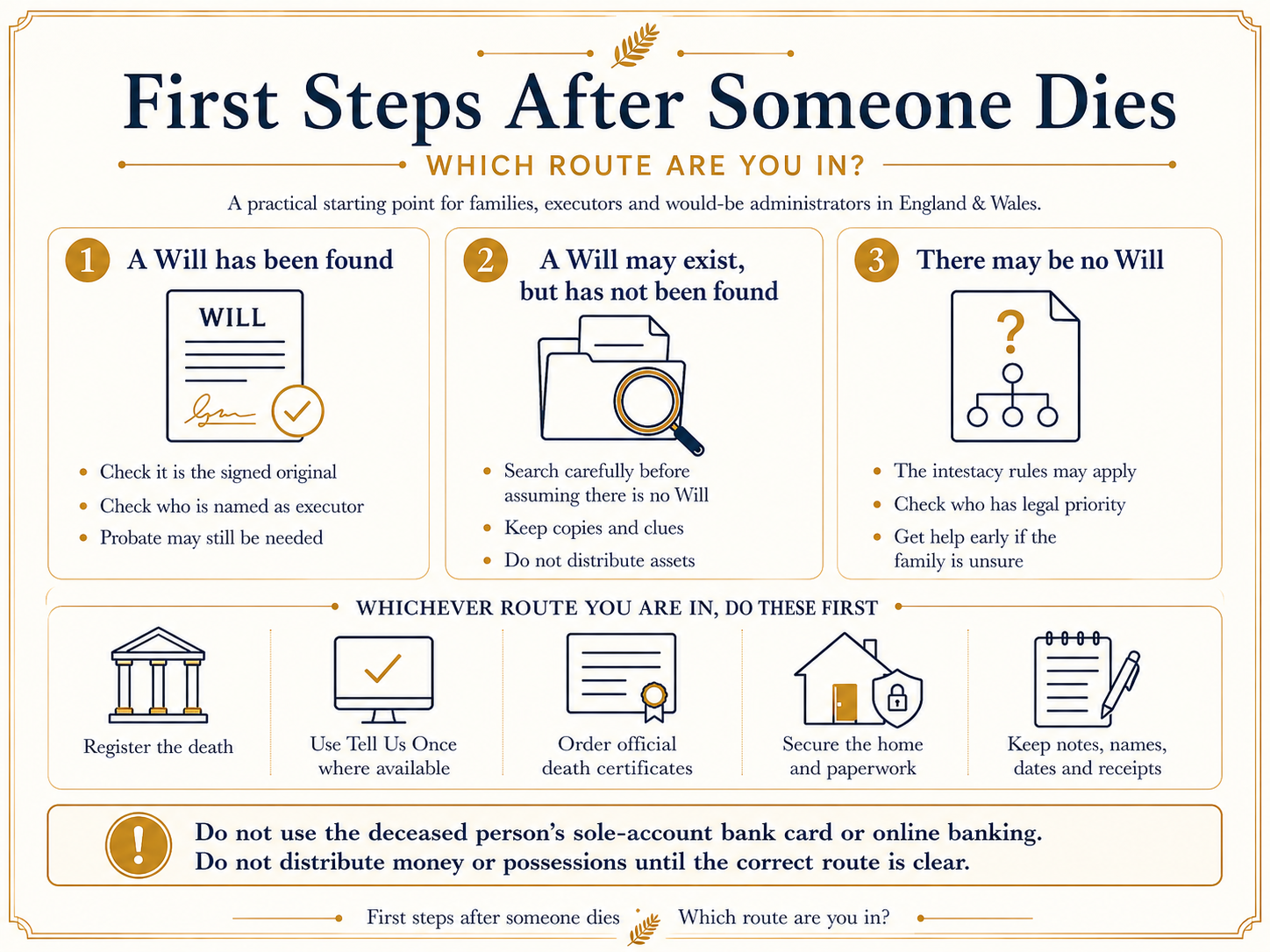

Which situation are you in?

Most families fall into one of three starting positions.

1. A Will has been found

This is often the clearest route, but it is not the end of the process. You still need to check whether it is the signed original Will, who is named as executor, whether probate may be needed, and whether there are assets, debts, property, tax issues or lifetime gifts to investigate.

2. A Will may exist, but has not been found

Do not assume there is no Will just because it is not immediately visible. Search carefully, ask close family, check paperwork, and consider whether a solicitor, Will writer, storage provider or the Probate Registry may hold it.

3. There may be no Will

If no Will exists, the estate may need to be handled under the intestacy rules. That changes who has authority to deal with the estate and who inherits. The most organised person is not automatically the right person to act.

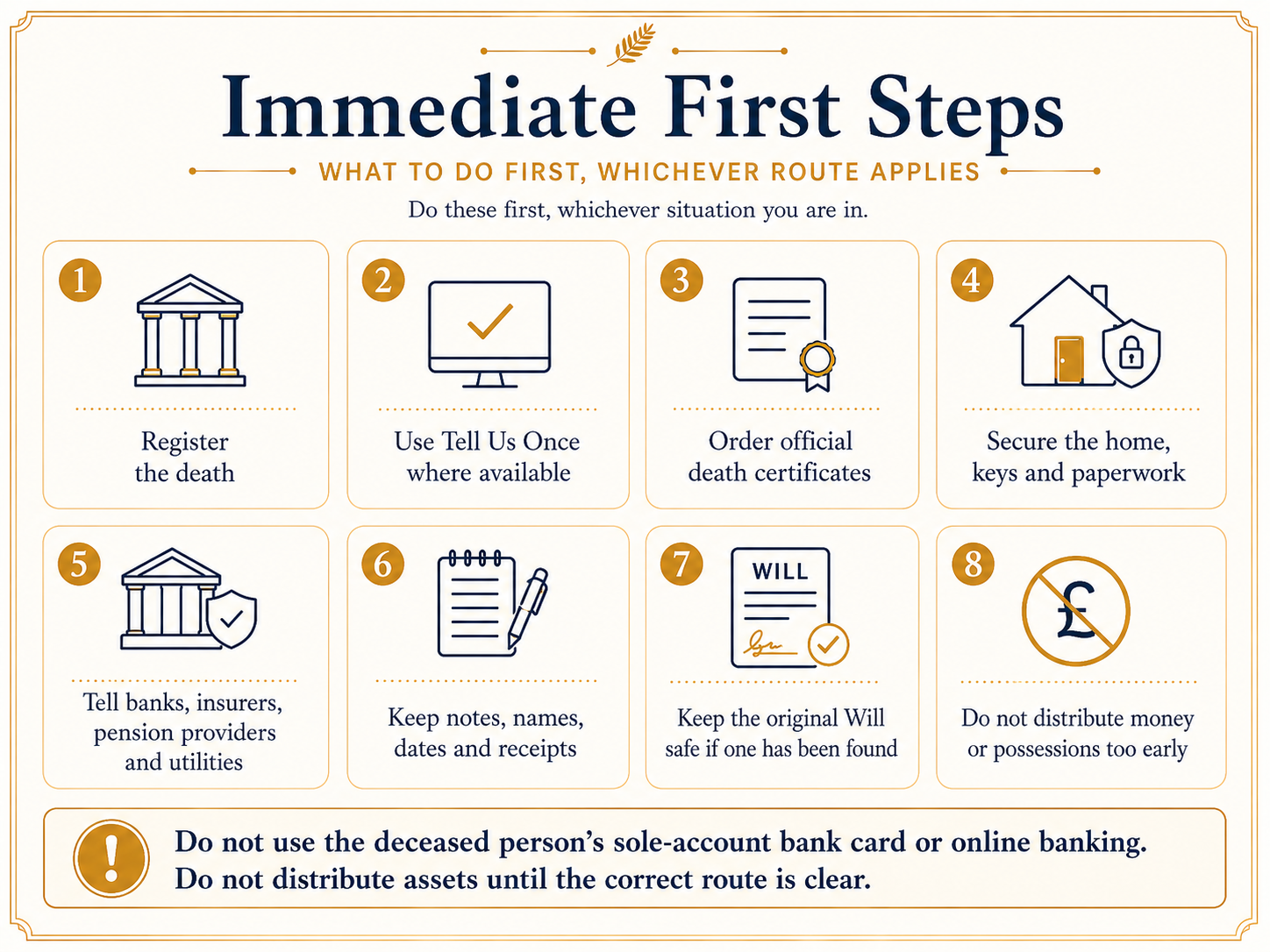

Do these first, whichever route applies

The key points are also set out below in text for clarity and accessibility

It is easy to feel that everything has to be done immediately. It does not. The first job is to protect the estate and gather information.

- Register the death.

- Use Tell Us Once where available.

- Order several official death certificates.

- Secure the home, keys, paperwork, valuables and vehicles.

- Tell banks, insurers, pension providers, utility companies and other relevant organisations.

- Keep notes of calls, dates, names, reference numbers and receipts.

- Keep the original Will safe if one has been found.

- Do not remove staples or bindings from the Will.

- Do not write on or alter the Will.

- Do not use the deceased’s sole-account debit card, PIN or online banking just because you know the details.

- Do not start distributing money, jewellery, furniture or possessions because you think you know what the Will says.

Before asking for help, gather these details if you can

- Full name of the person who has died.

- Date of death.

- Last address.

- Your relationship to them.

- Whether a Will has been found.

- Whether the Will is the signed original or only a copy.

- Who is named as executor, if known.

- If no Will has been found, who the closest relatives are.

- Whether there is a property.

- Whether anyone is living in the property.

- Whether there are bank accounts, investments, shares, pensions, business interests or life policies.

- Whether there are known debts, loans, care fees, tax issues or funeral costs.

- Whether there were significant gifts or transfers in the last seven years.

- Whether anything is urgent, such as an empty property, insurance, family disagreement, funeral funding or business responsibilities.

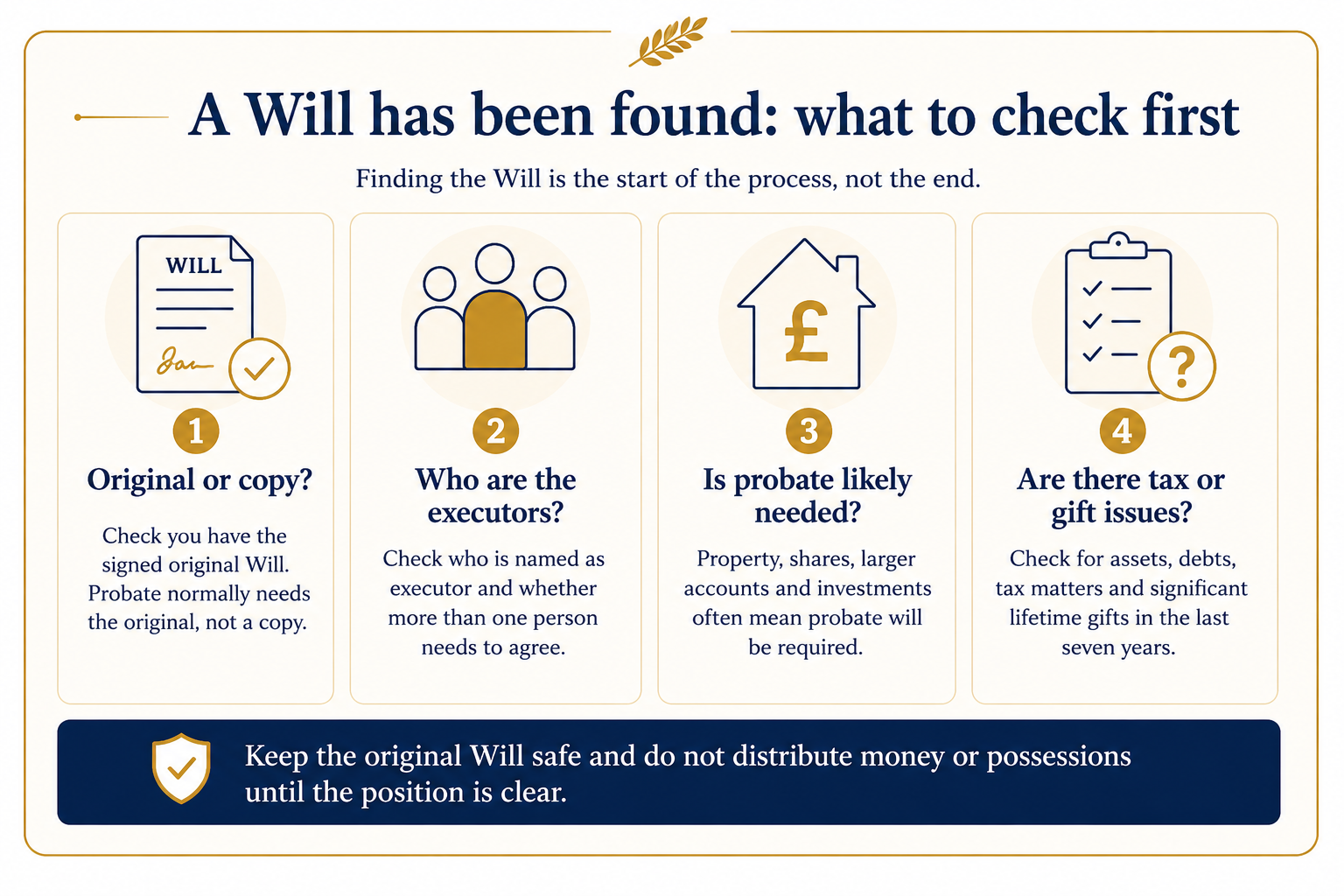

A Will has been found

Finding a Will is a good start, but it does not automatically mean the estate is simple or that everything can be dealt with straight away.

Finding a Will is only the start: check the original, the executors, probate and any tax or lifetime-gift issues.

The key points are explained below in more detail:

The first question is whether you have the signed original Will, not just a photocopy, scan or old draft. Keep it safe. Do not remove staples, bindings or covers. Do not write on it, mark it, amend it or attach notes to it.

Your next priorities are usually:

- Check who is named as executor.

- Check whether there are any codicils or later Wills.

- Keep the original Will safe.

- Register the death and use Tell Us Once where available.

- Order enough official death certificates.

- Make a first list of the main assets, debts and organisations involved.

- Secure any empty property and tell the insurer if the home is vacant.

- Keep notes of what has been done and what still needs checking.

- Avoid distributing money or possessions until the position is clearer.

If you are named as executor, you may be the person who can apply for probate and deal with the estate. If more than one executor is named, the executors may need to agree who will apply and how the work will be handled.

If you are unsure whether you want to act as executor, take advice before doing more than urgent protective steps. Once an executor starts dealing with the estate in a substantive way, stepping back can become more complicated.

Do not assume probate is unnecessary

Some small estates can be dealt with without probate, but many estates still need it. Probate is more likely to be needed where there is:

- a house or flat to sell or transfer;

- bank or investment accounts above the provider’s own threshold;

- shares or investment holdings;

- business interests;

- disagreement between family members;

- uncertainty about the Will;

- inheritance tax forms or reporting issues.

GOV.UK says probate is the legal right to deal with someone’s property, money and possessions after death. It also says the original Will is needed for a probate application and that a photocopy cannot be used.

Start a simple estate file

Before making decisions, start a basic estate file. This can be a folder, notebook, spreadsheet or document pack.

Record:

- the death certificate details;

- where the original Will is held;

- who the executors are;

- bank accounts and savings;

- property details;

- investments and shareholdings;

- pensions and life policies;

- debts, loans and regular bills;

- funeral costs;

- important calls, dates and reference numbers;

- documents still missing.

This does not have to be perfect on day one. The aim is to avoid losing information, duplicating work, or relying on memory.

Check whether there were significant lifetime gifts

Executors should not assume the estate is only what exists on the date of death. For Inheritance Tax purposes, gifts made in the seven years before death may also matter.

Executors may need to check gifts made in the seven years before death, not just the assets owned on the date of death.

This can include money, property, land, buildings, personal possessions, stocks and shares, or selling something for less than it was worth.

A one-year look through bank statements may not be enough if there were significant gifts, loans, transfers or financial help to family members. Executors may need to check further back, keep proper records, and take advice if the gifts are large, unclear, repeated, connected with trusts, or linked to an asset the deceased continued to benefit from.

Useful questions include:

- Were large cash gifts made to children, grandchildren or others?

- Were house deposits, loans, cars, business support or regular payments provided?

- Were any loans later written off?

- Were any assets transferred for less than market value?

- Did the deceased give away property or shares?

- Did they continue to use or benefit from anything they had given away?

This is not about making every small birthday or Christmas gift complicated. It is about making sure significant gifts are not missed.

You can read the GOV.UK overview here: Inheritance Tax and gifts.

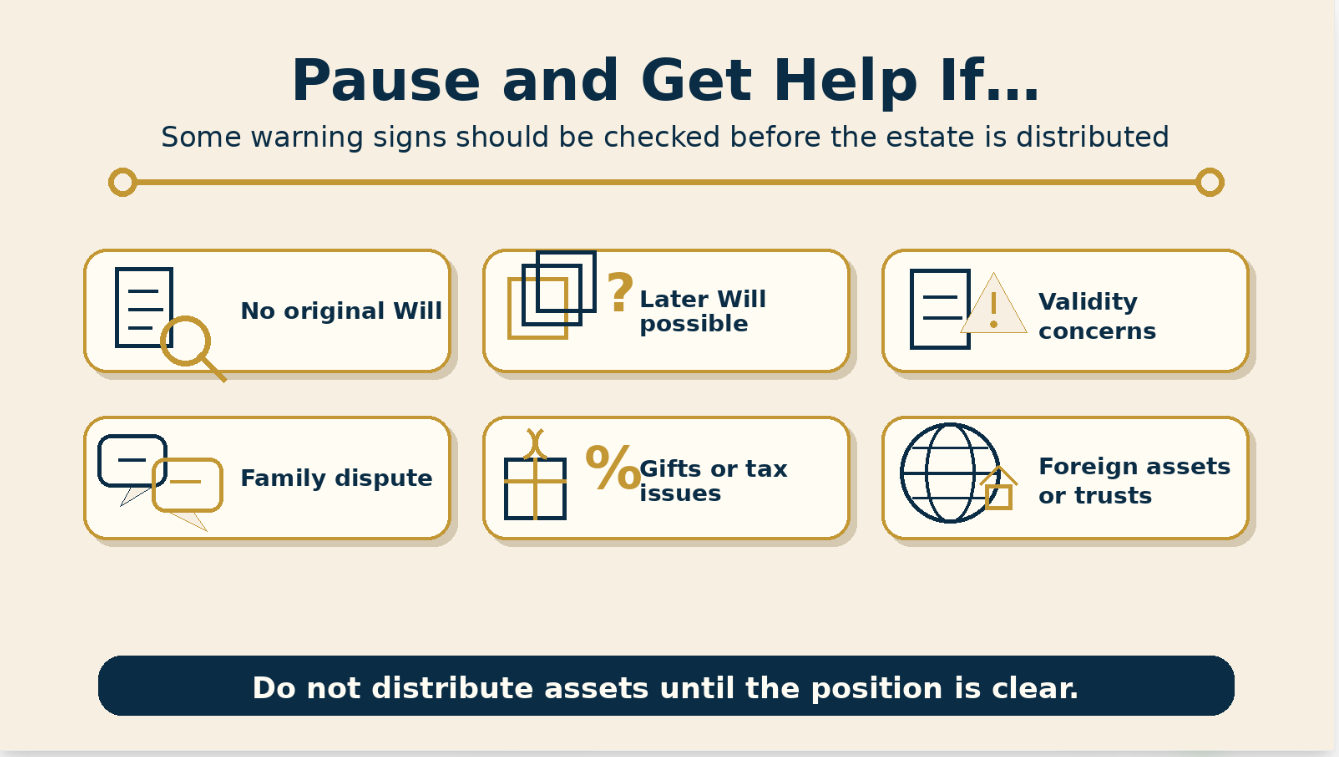

When to get help early

You may not need paid probate support for every estate. But it is sensible to get help early if:

- you only have a copy of the Will;

- the original Will is damaged, marked, unstapled or uncertain;

- there is more than one possible Will;

- executors disagree or do not communicate well;

- there is a property to sell;

- there are shares, investments or business interests;

- there were significant lifetime gifts in the last seven years;

- there may be inheritance tax reporting;

- family members are pressing for early distributions;

- you are unsure who has authority to act.

If this is your situation, the next step is to work through an executor checklist before applying for probate or distributing assets.

Next: A Will has been found: executor first steps before probate.

A Will may exist, but has not been found

This is one of the most common ways an estate becomes delayed, more stressful and more expensive than the family expected.

Do not assume there is no Will simply because it is not immediately obvious. Many people keep Wills in old files, boxes, drawers, safes, solicitor packets, storage facilities or with paperwork that does not look important at first glance.

If you think there may be a Will, start by searching carefully.

Check:

- the person’s home;

- filing cabinets, drawers, boxes and folders;

- safes, lockboxes and document wallets;

- old letters, emails and paperwork from solicitors or Will writers;

- bank paperwork or safe-custody references;

- family paperwork held by a spouse, partner, child or trusted relative;

- whether a solicitor, Will writer, accountant or storage provider was used;

- whether the Will may have been stored with the Probate Registry.

If you find a copy of a Will, keep it. It may help show who prepared the Will, when it was made, and where the signed original might be. But a copy is not the same as the original.

For a normal probate application, the signed original Will is required. If only a copy is available, the estate may still be resolvable, but extra evidence and a more careful process may be needed.

Do not rush into intestacy

If a Will might exist, do not rush to deal with the estate as if there is no Will.

That can cause problems if a valid Will is found later. The Will may name different executors, different beneficiaries, funeral wishes, guardians, trusts or gifts that nobody knew about.

Before assuming there is no Will:

- search properly;

- speak to close family;

- check with professional advisers;

- check storage providers;

- keep copies and clues;

- avoid distributing assets;

- keep written notes of what has been checked.

If there are several possible Wills, old copies, handwritten notes, unsigned drafts or uncertainty about which document is valid, get advice before anyone acts on assumptions.

If the original Will cannot be found

A missing original Will does not always mean there is no Will, but it does make the estate more complicated.

The family may need to work out:

- whether the Will was deliberately revoked;

- whether the original was lost accidentally;

- whether a later Will exists;

- whether a copy can be proved;

- who is entitled to apply;

- whether specialist probate help is needed.

This is not usually the point to guess or “just carry on”. If the original Will cannot be found after proper checks, take advice before applying for probate or distributing assets.

There may be no Will

If no Will has been found, the estate may need to be dealt with under the intestacy rules.

That does not mean the most organised person can simply take over. Where there is no Will, the person with legal priority usually applies to become the administrator of the estate. In many families, that may be the spouse or civil partner first, followed by adult children.

A friend, sibling, neighbour or more distant relative may be very helpful in practice, but that does not automatically mean they have authority to deal with the estate.

Work out who has priority

Before anyone starts administering the estate, try to identify:

- whether the person was married or in a civil partnership;

- whether they had children;

- whether any children have died leaving children of their own;

- whether there are surviving parents, siblings or other relatives;

- whether there are unmarried partners, stepchildren or blended-family complications;

- whether anyone is already dealing with banks, property or paperwork;

- whether there is any disagreement about who should act.

The intestacy rules can surprise families. Unmarried partners, stepchildren, close friends and carers do not automatically inherit just because they were important in the person’s life.

First priorities where no Will is found

The practical first steps are usually:

- keep searching for any Will or evidence of one;

- secure the home, keys, valuables and paperwork;

- register the death and use Tell Us Once where available;

- order official death certificates;

- make a rough list of assets, debts and organisations;

- identify who appears to have legal priority;

- avoid promising anyone that they will inherit;

- avoid distributing money, possessions or sentimental items too early;

- keep written notes of what has been checked.

When no-Will estates need extra care

Get advice early if:

- the person had an unmarried partner;

- there are children from different relationships;

- there are stepchildren or informal family arrangements;

- relatives disagree about who should act;

- someone has already started dealing with the estate without clear authority;

- there is a property to sell;

- there are significant investments, shares or business interests;

- there were significant lifetime gifts;

- the family is unsure who inherits under the intestacy rules.

No-Will estates can be straightforward, but they can also become difficult quickly if the wrong person starts acting, assets are distributed too soon, or family members assume the rules match what the deceased “would have wanted”.

Common pressure points

Some estates are small and simple enough for family members to deal with themselves. Others look simple at first, but become more difficult once the paperwork is checked.

Common pressure points include:

- the original Will cannot be found;

- only a copy of the Will is available;

- there is no Will;

- there is a property to secure, insure, sell or transfer;

- there are shares, investments or business interests;

- there are several banks, pensions or financial organisations to contact;

- there were significant gifts, loans or transfers in the last seven years;

- family members disagree about who should act or what should happen;

- someone is pressing for money or possessions to be distributed quickly;

- there are tax forms, valuations or HMRC questions to deal with;

- the person who seems responsible does not have the time, confidence or paperwork skills to manage the process.

The difficulty is that families often do not know whether an estate is simple until they have started checking. A house, share certificates, missing paperwork, lifetime gifts or family disagreement can change the position quickly.

When to get help early

You do not always need paid support. But it is sensible to get help before mistakes are made if:

- you are unsure whether you have authority to act;

- you are named as executor but do not know whether you want to take on the role;

- more than one executor is named and you do not agree how to proceed;

- the Will is missing, damaged, marked, unstapled or uncertain;

- there is no Will and the family is unsure who has priority;

- there is a property involved;

- the estate includes shares, investments, business interests or trusts;

- there were significant lifetime gifts;

- inheritance tax reporting may be needed;

- beneficiaries are already in disagreement;

- you are worried that acting now may make it harder to step back later.

Getting help early does not always mean handing over the whole estate. Sometimes it simply means checking the correct route, understanding who has authority, and avoiding avoidable mistakes before the estate administration goes too far.

Practical middle ground

Many families want to stay involved but need help with the process. That is often a sensible middle ground.

You may be able to deal with some parts yourself, such as gathering paperwork, securing the home, listing accounts and keeping family notes. You may still want professional help with the probate application, tax reporting, property issues, missing Will problems, executor disagreement or final estate accounts.

The aim is not to make the process more complicated. The aim is to make sure the right person is acting, the right records are kept, and the estate is not distributed before the legal and tax position is clear.

Banks, frozen accounts and funeral costs

Tell Us Once is useful, but it does not deal with everything.

It can notify many government organisations, including HMRC, DWP, the Passport Office, DVLA and local councils. But banks, mortgage providers, insurers, utility companies, landlords, private pension providers and other financial organisations usually need to be contacted separately.

Once a bank is told that someone has died, it will usually freeze sole accounts. That is normal. It helps protect the estate and prevents money being withdrawn without the correct authority.

Do not use the deceased person’s sole-account debit card, PIN or online banking after death, even if you know the details and even if you believe the money will eventually be used properly. Keep the process clean and documented.

How funeral costs may be handled

Funeral costs are often one of the first practical worries.

In some cases, a bank may agree to pay a funeral invoice directly from the deceased person’s account. This usually depends on the bank’s own process and the documents provided, such as the death certificate and the funeral director’s invoice.

Before paying funeral costs personally, it is worth asking the bank what its bereavement process allows.

Keep:

- the funeral estimate;

- the final funeral invoice;

- receipts for anything paid personally;

- notes of calls with banks or funeral directors;

- details of who paid what and when.

If someone pays funeral costs personally, they should keep clear evidence. Funeral costs are normally treated as an estate expense, but the executor or administrator should still keep proper records before reimbursing anyone.

Joint accounts

Joint accounts are different from sole accounts. The surviving joint account holder may still be able to use the account, but the bank still needs to be told about the death.

Do not assume that every account, investment or policy works the same way. Banks, building societies, investment platforms, pension providers and insurers each have their own bereavement process and their own evidence requirements.

Some situations should be checked before executors distribute assets or make irreversible decisions.

Practical record to keep

For each organisation contacted, record:

- organisation name;

- account or reference number;

- date contacted;

- person or department spoken to;

- documents requested;

- documents sent;

- whether probate is required;

- next action and deadline.

This simple log can prevent confusion later, especially where several family members are helping or where more than one executor is named.

Need help with this estate now?

If you are facing a missing Will, no Will, uncertainty about who should act, pressure from family, property issues, paperwork, banks, investments or possible tax reporting, you do not have to carry the whole process alone.

Fern Wills & LPAs does not provide full probate administration in every case, and this page is not personal probate advice. But we can help you understand the position, identify the next sensible step, and decide whether you may need specialist probate or tax support.

See: Probate (Executor Support)

You can also contact us here: Contact Fern Wills & LPAs

If you contact us, it helps if you can first gather:

- the full name of the person who died;

- their date of death;

- their last address;

- your relationship to them;

- whether a Will has been found;

- whether the Will is the signed original or only a copy;

- who is named as executor, if known;

- whether there is a property;

- whether anyone is living in the property;

- a rough list of known assets and debts;

- details of any banks, shares, investments, pensions or business interests;

- whether there were significant lifetime gifts, loans or transfers;

- whether anyone else is already acting or believes they should act;

- what feels urgent.

Helpful related pages

You may also find these useful:

- Choosing an Executor: what they do and how to pick the right one

Useful if this situation has made you think about who you have chosen to deal with your own estate. - What to leave behind to make life easier for your executor

Useful if you want to reduce the paperwork burden for your own family later. - Document Storage

Useful if the main problem is that the signed original Will cannot be found, or you want to avoid that problem for your own family. - Life & Legacy Logs

Useful if you want a practical way to record property, finances, lifetime gifts, passwords, access routes or other details your family may need later. - Will & LPA MOT

Useful if your own Will, executors, LPAs or document storage may now need checking. - LPA MOT: Lasting Power of Attorney Review

Useful if a bereavement has made you realise that your own attorneys, replacements or LPA storage arrangements also need checking.

Make your own Will easier to find later

Many families only discover the weakness in an estate plan when someone dies and the original Will cannot be found.

Having a Will is not enough. It also needs to be current, signed properly, and findable when your family needs it.

Once the immediate situation is under control, it may be worth checking your own affairs:

- Is your Will up to date?

- Can the signed original be found?

- Do the right people know where it is stored?

- Are your executors still suitable?

- Do your executors still get on well enough to act together?

- Have your circumstances, family or assets changed?

- Have you made significant lifetime gifts that should be recorded?

- Would your family know where to find your key financial information?

A small amount of organisation now can prevent delay, uncertainty and stress for your family later.

Final note

This guide is intended to help you take the first sensible steps after someone dies. It is not a substitute for probate advice, tax advice or legal advice on a disputed estate.

If anything is unclear, disputed, high-value, tax-sensitive or urgent, get help before distributing assets or making decisions that may be difficult to undo.