Right to Occupy (RTO)

Last verified: March 2026 (England & Wales)

You may want a partner, friend, or relative to keep living in your home after you die, but you still want the property to pass to your chosen beneficiaries. A right-to-occupy trust in your Will lets someone live in your property for a set period or for life, without giving them the house outright.

For this article, we use the term “right to occupy”. In some Will wording, you may see “right to reside” or “right of residence” instead. In practice, they usually refer to the same basic idea.

Quick-read summary

• A right-to-occupy trust in your Will can give a named person the legal right to live in a specific property (or your share of it).

• It can continue for life, for a fixed period (months or years), or until a trigger event (for example, remarriage or moving out)

• It can set out who pays which costs: bills, insurance, repairs, mortgage, and service charges.

• It can ring-fence the property so that, when the right ends, it passes to your chosen beneficiaries rather than being left to chance.

A right-to-occupy trust can help you look after someone you care about now, without leaving the future of your home to chance.

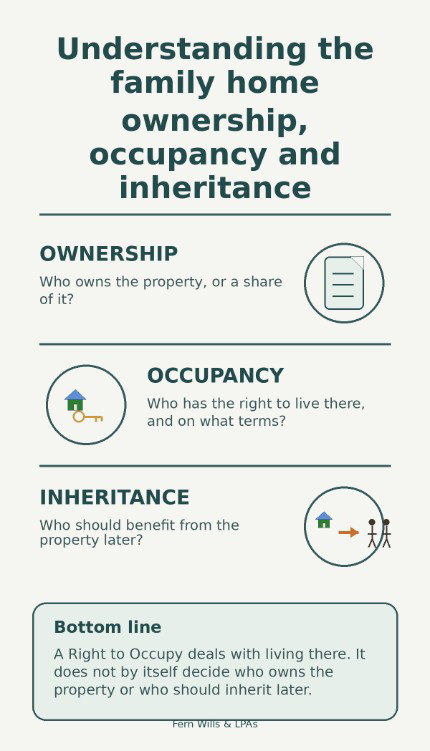

A right-to-occupy trust separates “who lives there now” from “who inherits later”.

Right to Occupy is usually a narrower tool, not the default answer for every family-home case.

If the real aim is longer-term security for a surviving partner together with stronger protection and flexibility across two deaths, a Property Life Interest Trust or another Will-trust structure may be the better fit.

This article explains Right to Occupy on its own terms, but the better starting point is the family outcome you want, not the label.

What is a right-to-occupy trust?

A right-to-occupy trust is usually created by your Will. Instead of leaving the property outright to one person, you can:

• place the property, or your share of it, into a Will trust

• give a named person the right to live there on terms you set

• decide who should inherit once that right to occupy has ended

The person living in the property is often called the “life tenant” or “occupier”. The people who inherit when their right comes to an end are the “ultimate beneficiaries”.

How it works in practice

- You make a Will that includes a right-to-occupy trust for a particular property (or your share).

- When you die, your executors transfer that property into the trust instead of leaving it outright to any one person.

- The trustees hold the property and must honour the occupier’s right to live there, as long as they keep to the conditions you set.

- You decide how long the right lasts:

• for the rest of the occupier’s life, or

• for a fixed period (for example, 6 months, 12 months, or 3 years), or

• until a trigger event (for example, they remarry or move out permanently). - You also decide who pays which costs: day-to-day bills, insurance, routine repairs, and any mortgage or service charges.

- When the right ends, the property passes to your chosen ultimate beneficiaries, such as your children.

You decide the rules while you are alive; your trustees simply follow them when the time comes.

Ownership: sole owner, joint owners, and “tenants in common”

How your home is owned matters.

• Sole owner

If you are the only owner, your Will can give someone a right to occupy your home and then pass it to your chosen beneficiaries when that right ends.

• Joint owners as “beneficial joint tenants”

If you own the property as beneficial joint tenants, your share normally passes automatically to the surviving owner outside the Will. A right-to-occupy clause in your Will over that share will not bite, because there is nothing left in your estate to go into the trust.

• Joint owners as “tenants in common (usually 50–50, but the shares can be anything from 99–1)”

To use a right-to-occupy trust over your share on first death, the joint ownership usually needs to be changed to “tenants in common” first. That way, your own share can follow the instructions in your Will.

Different ownership splits can have tax consequences, especially where the property is an investment and you are sharing rental income, so tailored advice is important.

In many cases this involves:

• a severance of joint tenancy, and

• a Form A restriction being added to the Land Registry title so it is clear the property is held as tenants in common, and

• checking whether there is already a Declaration of Trust in place and, if so, how that interacts with your Wills (see separate article on Declarations of Trust).

How your home is owned on paper decides whether a right-to-occupy clause in your Will can actually work in practice.

Getting the ownership structure right is just as important as getting the Will wording right.

Cases

Real families don’t fit a one-size-fits-all template. The same trust shape can be adapted to very different situations.

Sole owner with an unmarried partner and children from a previous relationship

Sarah owns her house in her sole name. Her partner, Mark, lives with her, and she has two adult children from a previous relationship.

Without a right-to-occupy trust, Sarah faces a difficult choice:

• Leave the house to her children and risk Mark having no security, or

• Leave the house to Mark and hope he later “does the right thing” for the children.

With a right-to-occupy trust in her Will, Sarah gives Mark the right to live in the property for life (or until he moves out), with her children named as the ultimate beneficiaries. Mark has a secure home; the children know they will inherit the property in the end.

Joint owners, blended families, and tenants in common

Ian and Louise each have children from earlier relationships. They own their home together. They change the ownership to tenants in common (usually 50–50, but with the option to choose different shares if needed) and update their Wills.

Each Will:

• Puts that person’s share into a right-to-occupy trust for the survivor, and

• Names their own children as the ultimate beneficiaries of that share.

If Ian dies first, Louise keeps the right to live in the property under his trust, and still owns her own share. When Louise later dies or moves out, Ian’s children inherit his share and Louise’s children inherit hers. The survivor has security; both sets of children are protected.

Later-life partnership where both have their own properties

David and Helen are in a long-term relationship, on their second marriages. Each is financially independent and owns their own property. They live mainly in David’s house but Helen keeps her flat as a “back-up”.

David wants Helen to be able to stay in his home if he dies first, but only for a sensible period so she can decide whether to move back to her own flat or buy somewhere new.

His Will creates a right-to-occupy trust giving Helen:

• The right to live in his house for up to 12 months after his death (six months is a common choice), and

• Clear rules about bills, insurance, and repairs.

After that period (or earlier if Helen moves out), the house is sold and the proceeds pass to David’s children. Helen has time and breathing space; David’s children still receive the value of the property.

A right-to-occupy trust can give a new partner breathing space without permanently diverting the family home away from your children.

Supporting an adult child without locking in the property forever

Mrs Patel owns her home outright. Her son, Ravi, lives with her and is building up his career; her daughter, Meera, owns her own home.

Mrs Patel wants Ravi to be able to stay in the house for a while after she dies, but does not want the house tied up indefinitely. Her Will gives Ravi the right to occupy for up to five years, provided he pays the household bills and keeps the property in good condition.

At the end of that period, or when Ravi moves out, the house is sold and the proceeds are shared between Ravi and Meera in the proportions Mrs Patel chooses. Ravi gets the stability he needs; both children share in the value.

Right to occupy, working alongside a Declaration of Trust

Alice and Bob buy a house together. They sign a Declaration of Trust confirming that they own the property as tenants in common (usually 50–50, but adjusted here so Alice owns a larger share because she provided most of the deposit). The Declaration of Trust sets out their respective shares and what happens to the sale proceeds if they later sell.

Alice also makes a Will. Instead of leaving her share of the house directly to her daughter, Clara, she:

• Leaves her share on a right-to-occupy trust for Bob, so he can go on living in the property after her death, and

• Names Clara as the ultimate beneficiary of her share once Bob’s right to occupy ends.

If Alice dies first, Bob carries on living in the property under the terms of the right-to-occupy trust, and Clara knows she will eventually inherit Alice’s share. The Declaration of Trust continues to govern the overall shares in the property; the Will trust governs who can live there and who ultimately benefits from Alice’s portion.

A Declaration of Trust records “who owns what”; a right-to-occupy trust sets out “who can live there now and who inherits later”.

Key points to agree when setting up a right-to-occupy trust

When we draft this type of clause or trust within a Will, we will usually talk through:

• Who should have the right to occupy (partner, friend, relative).

• Which property is covered (your main home, a specific rental, or your share only).

• How long the right should last: life, a fixed period, or until a trigger event.

• What counts as moving out permanently or no longer using it as a main home.

• Who pays which costs: utilities, council tax, ground rent, service charges, repairs, and any mortgage.

• Whether the trustees should ever be able to sell and buy another suitable property for the occupier, and on what terms.

• Who the ultimate beneficiaries are once the right ends.

• Whether another trust shape (for example, a Property Life Interest Trust or a more flexible family trust) might better suit what you are trying to achieve, so you are choosing the structure that really fits you.

The aim is to make sure the trust structure fits your family and your goals.

Trustees, registration, and ongoing responsibilities

A right-to-occupy clause usually means trustees hold the property once your Will takes effect. They must:

• Look after the property and follow the trust terms.

• Balance the needs of the occupier and the ultimate beneficiaries.

• Take advice on any tax or registration requirements that apply at the time.

There are detailed rules on when trusts must be registered with HMRC and how any tax is reported, and those rules can change. Your executors and trustees should take specialist advice at the time the trust actually has to be operated.

For ethical and governance reasons, Fern Wills & LPAs does not take trustee appointments or create standalone lifetime trusts. However, Fern Wills & LPAs does create trusts that arise on death within Wills. Fern Wills & LPAs does not register trusts. Where a trust needs to be operated or registered, we will introduce you to an appropriate specialist to act and administer the trust. You remain free to choose your own adviser.

Is a right-to-occupy trust right for you?

A right-to-occupy trust is one tool among many. It may be worth exploring if:

• You live with a partner you are not married to or in a civil partnership with.

• You have children from a previous relationship and want to protect their eventual inheritance.

• You own a property in your sole name and want a partner or relative to have a home for a period, but not necessarily the property outright.

• You and your partner each have your own children, your own assets, or your own properties, and want a fair balance between security for each other and protection for your families.

You are not expected to read this and choose a product by label. The best starting point is a conversation about what you want to achieve: who you want to protect now, who you want to provide for later, and how flexible you want things to be.

This article is general information only, not individual advice.

If you’d like help applying this to your circumstances, we can guide you through the options.

Related Fern Wills & LPAs articles

• Property Life Interest Trust (PLIT)

If you are deciding between a simple Right to Occupy and a fuller home-protection trust, the next step is a short conversation about three things: who needs security now, who should inherit later, and how much flexibility the trustees may need.

We can talk that through in plain English and then recommend the trust structure that best fits your family, rather than forcing you into a label too early.