How Pensions Affect Inheritance Tax

Last verified: July 2026 (England & Wales)

For many families, pensions used to feel separate. Your home was one thing. Your savings and investments were another. Your pension sat in its own box.

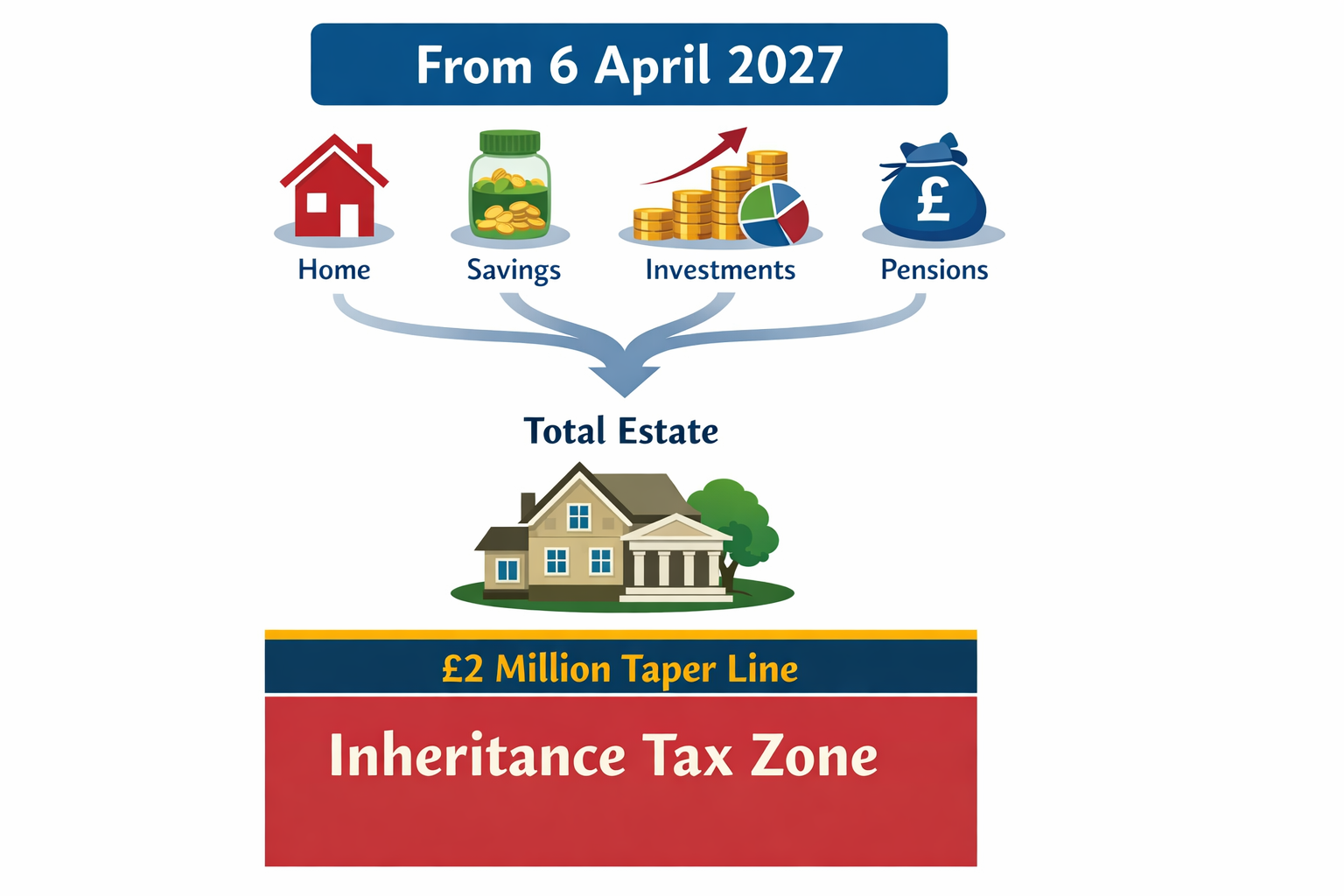

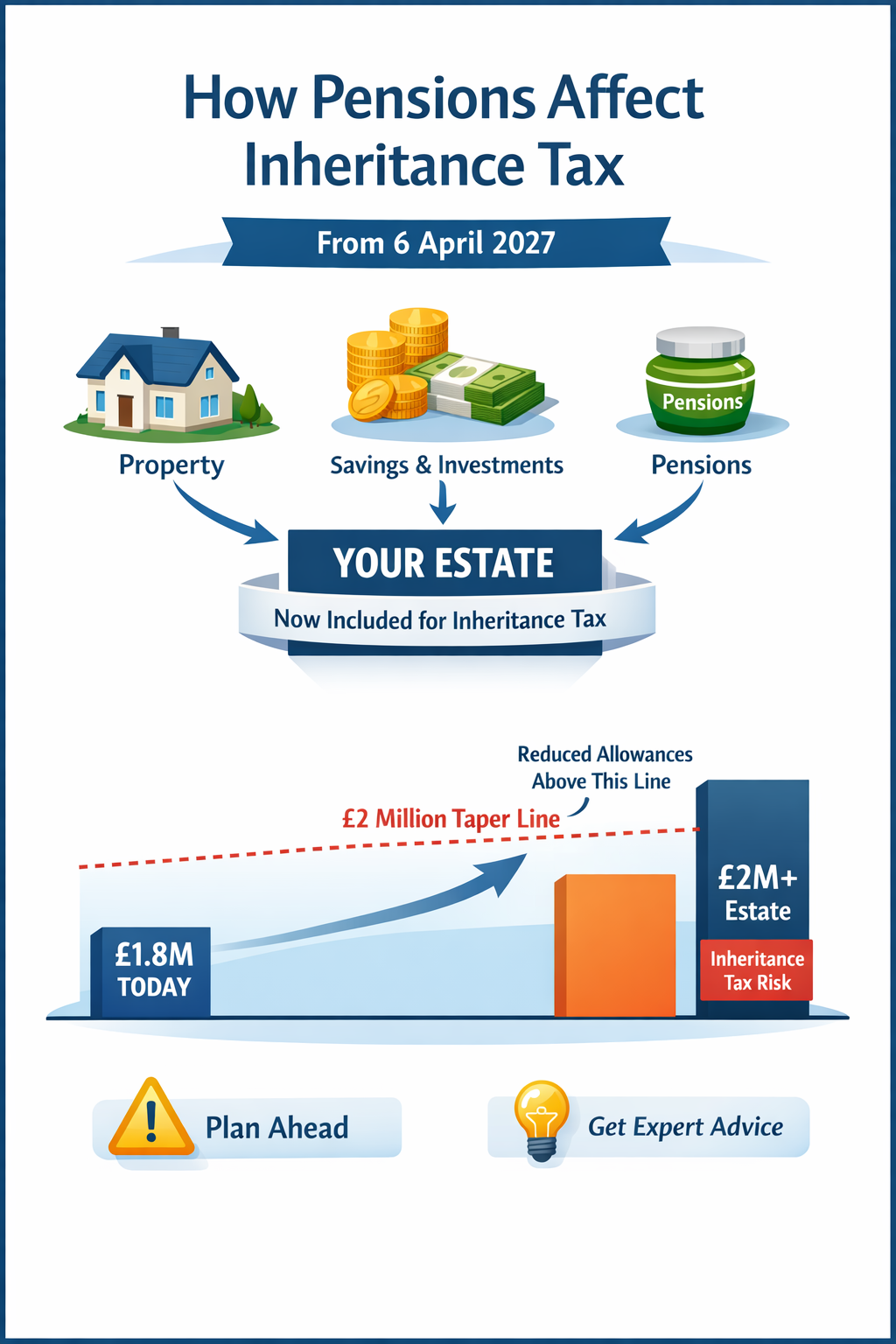

From 6 April 2027, that becomes much harder to assume.

If you have a larger estate, a valuable home, strong pensions, or a combination of all three, pensions may now have a direct impact on your inheritance-tax position. For some families, that could mean a bigger tax bill. For others, it could mean being pushed into inheritance-tax planning earlier than expected.

That is why this is no longer just a pensions issue. It is an estate-planning issue.

Quick-read summary

- From 6 April 2027, most unused pension funds and pension death benefits will be brought into scope for Inheritance Tax.

- That matters most for families whose overall wealth may already be near the key thresholds once pensions are included.

- The £2 million line matters because the Residence Nil Rate Band (RNRB): rules & how to claim can taper away above that level.

- Some families may face both inheritance tax and later income tax on inherited pension funds, especially where death occurs after age 75. In a narrow worst-case example, the combined effect can reach 67%, but that is not automatic and should not be treated as a fixed pension tax rate.

- Good planning is usually not one clever trick. It is a joined-up use of the right tools: Will planning, trust planning, ownership planning, gifting, pension nominations and financial advice.

- Fern Wills & LPAs can help with the legal and estate-planning side and, where pensions are involved, work alongside your financial adviser or introduce you to one.

Why this matters now

Many families do not think of themselves as being in inheritance-tax territory.

They may have a good house, decent savings, a few investments, and sensible pensions, but they still feel a long way from a tax problem.

That is exactly why this change matters.

Once pensions are added back into the picture, some estates that looked manageable may suddenly sit much closer to the key thresholds than expected. In practice, that means more families should stop looking at pensions in isolation and start looking at the estate as a whole.

For the wider inheritance-tax background, see our guides on £1 Million Tax-Free and What Is the 7-Year Inheritance Tax Rule? A Plain-English Guide explain other important parts of the inheritance-tax framework.

The more valuable the pension, the more important it is that the legal plan and the financial plan match.

What changes from April 2027

From 6 April 2027, most unused pension funds and pension death benefits will be included in the value of the estate for Inheritance Tax purposes. That does not mean every family will suddenly pay Inheritance Tax on a pension.

It does mean that pensions can no longer safely be treated as a separate, sheltered family asset for Inheritance Tax purposes.

There are still important distinctions. For example, death-in-service benefits from registered pension schemes will remain outside the estate for Inheritance Tax purposes. The result can also depend on the type of pension benefit, the age at death, who receives it and the law in force at the time.

Personal representatives will be responsible for identifying relevant pension assets, obtaining information from pension schemes, and reporting and paying any Inheritance Tax due. HMRC is still finalising the supporting information-sharing regulations and guidance ahead of April 2027.

That makes clear pension records and up-to-date provider details more important for executors as well as for lifetime planning.

Why the £2 million line matters more now

For many larger estates, the real pressure point is not just inheritance tax in general. It is the interaction between pensions and the £2 million taper threshold.

If a qualifying home passes to direct descendants, the Residence Nil Rate Band (RNRB): rules & how to claim can add valuable extra allowance. But once an estate goes above £2 million, that allowance starts to taper away.

That is where pensions can suddenly make a major difference.

A family who looked comfortably below £2 million when counting only the home, savings and investments may look very different once unused pension wealth is added in.

A family sitting at about £1.8 million today may not think they need inheritance-tax planning yet. But modest growth, plus pensions, can move the picture surprisingly quickly.

As a simple illustration, an estate worth about £1.8 million today could reach £2 million in only a few years with modest growth. If pensions and death benefits are also material, the review should happen sooner, not later.

What people mean by the “67% tax” point

You may now hear people talk about a “67% tax” on inherited pensions.

That is not a fixed tax rule. It is shorthand for a severe combined-tax outcome in a particular kind of case.

The basic idea is this. From 6 April 2027, most unused pension funds and pension death benefits are due to be brought into the estate for inheritance-tax purposes. If inheritance tax applies at 40%, that can reduce the pension value first. If the remaining pension benefit is then drawn by a beneficiary who pays income tax at 45%, the combined effect can leave only 33% of that part of the fund.

That is where the 67% headline comes from.

But it is only an illustration. It depends on the estate being taxable, the type of pension benefit, the age at death, who receives the benefit, whether any exemption applies, and the beneficiary’s own income-tax position.

For many families, the rate will not be 67%. For some, there may be no extra inheritance tax at all. The real point is not the headline number. The real point is that pensions, Wills and financial advice now need to be reviewed together.

Fern Wills & LPAs does not give pension, investment or regulated financial advice. We can help with the Will and estate-planning side, and we can work alongside your financial adviser or introduce you to one where appropriate.

Pensions are one of the clearest examples of why Will planning and financial advice need to speak to each other.

The planning tools people often consider

This is where many articles go wrong. They explain the problem, then stop.

In real life, families want to know what tools may be available.

The right answer depends on the numbers, the family and the client’s goals. But these are some of the tools people often consider as part of a joined-up estate plan.

Pension nominations and beneficiary planning

This is often the first area to review, but it sits firmly with a financial adviser.

A nomination does not rewrite the tax rules, but it can affect who receives the benefits, how smoothly the benefits are dealt with, and whether the wider family plan still makes sense.

If pensions are a meaningful part of your wealth, nomination forms should not be left on autopilot.

Could an equal Will still produce an unequal result?

A Will may leave the estate equally between two children. But suppose the client also has a £1 million pension and the current nomination favours only one child.

The Will may be professionally drafted and legally effective, yet the overall family outcome could be very different from what the client understood as equal treatment.

A Will usually controls the assets that pass through the estate. Pension death benefits are generally dealt with under the pension scheme’s rules.

Most pension providers or trustees will take the member’s nomination or expression of wishes into account, but they usually retain the final decision. The precise position depends on the scheme.

From 6 April 2027, the pension may also affect the estate’s Inheritance Tax calculation even though the Will may not decide who receives the pension benefits.

The practical question is not simply, “What does the Will say?” It is, “Do the Will, pension nominations and wider financial plan still produce the result the client actually wants?”

If pensions change the Inheritance Tax picture, the rest of the estate may also need to be structured more carefully. That can include the gifting pattern, flexibility between beneficiaries, trustee powers, how assets pass on first death, and whether the current Will still reflects what the family is trying to achieve.

Spouse and civil partner planning

For married couples and civil partners, part of the planning conversation may be about making proper use of spouse exemption and transferable allowances.

That does not remove the need to plan. It simply means the first death and second death should be looked at together, rather than treating each event in isolation.

For unmarried couples, the position is often much harsher, so careful planning becomes even more important.

Lifetime gifting

For some families, gifting remains part of the tool kit.

That may include Potentially Exempt Transfers or, in the right circumstances, gifts out of surplus income. The aim is not to give assets away blindly. The aim is to reduce future exposure without undermining the client’s own security and lifestyle.

If gifting is being considered alongside pension and inheritance-tax planning, it should be deliberate, affordable and properly recorded. The Lifetime Gifts Log can help record gifts made during lifetime, including the date, recipient, value, funding source, exemption or tax treatment, and where the supporting evidence is kept.

That record matters because executors may later need to show whether a gift falls within the seven-year rule, the normal-expenditure-out-of-income exemption, or another inheritance-tax treatment.

For one part of that picture, see What Is the 7-Year Inheritance Tax Rule? A Plain-English Guide.

Trust planning

Trusts are still relevant, but they should not be sold as a magic tax answer.

For many families, the main value of a trust is control, family protection, and keeping inheritance on track across two deaths. Tax may be part of the picture, but it is rarely the only reason the trust exists.

Depending on the family and the numbers, that may include a Flexible Life Interest Trust (FLIT) – The Modern Family Trust, a property-protection style trust, or in more specialist cases a Nil Rate Band Discretionary Trusts (NRBDTs).

The key point is this: use the right trust for the right reason, not because “trusts are good for tax”.

Severance of tenancy and ownership structure

If trust planning is part of the Will strategy, ownership matters.

In some cases, severance of joint tenancy may be needed so the trust can actually operate as intended. This is not an inheritance-tax relief by itself, but it can be a critical practical step if the overall estate plan is to work properly.

Charitable legacies

For some families, charitable giving is both a personal priority and a sensible planning tool.

Gifts to qualifying charities are generally exempt from inheritance tax, and in some cases leaving at least 10% of the relevant net estate to charity can reduce the inheritance-tax rate on the taxable part from 40% to 36%.

That said, charity planning has its own technical rules and drafting points, so it should be considered as part of the wider estate plan rather than treated as a quick fix.

See our guide to Charitable Gifts in Wills: the 10% Rule, the 36% Rate, and Why Older Clauses Need Reviewing.

Adviser coordination

This is one of the most important tools of all, and it is often the most overlooked.

The Will planner may understand the trusts and family dynamics. The financial adviser may understand the pensions, wrappers and withdrawal strategy. The accountant may understand another part again.

The best results usually come when those strands are coordinated rather than left in separate silos.

Good planning is rarely about one clever trick. It is about getting the moving parts to work together.

What Fern Wills & LPAs does, and what a financial adviser does

Fern Wills & LPAs can help with the legal and estate-planning side, including Wills, trust structures, ownership planning, severance issues, and how the estate should pass across the family.

A financial adviser should deal with the pension-specific side, including pension structure, wrapper selection, withdrawal strategy, beneficiary planning within the pension regime, and the wider retirement-planning consequences.

That distinction matters.

It protects the client. It keeps the advice joined up. And it avoids a very common problem, where somebody makes a legal move over here or a financial move over there without checking whether the two still fit together.

If you already have a financial adviser, we are happy to work alongside them.

If you do not, we can introduce you, with no obligation, to a financial adviser who understands the wider estate-planning picture.

If pensions are a material part of your estate, speak to your financial adviser. If you do not have one, we can introduce you to one who understands joined-up estate planning.

What to review now

If this topic may affect you, these are the questions worth asking now:

- What is the rough value of the whole estate once pensions and death benefits are included?

- Are you anywhere near the £2 million line once everything is counted?

- Are you married, in a civil partnership, or unmarried?

- Does your current Will still reflect what you want to happen on first death and second death?

- Are any trusts in the Will there for a clear reason, or are they just old wording that has never been revisited?

- Have your pension nominations been reviewed recently?

- If your Will aims to treat beneficiaries equally, do the pension nominations and likely pension benefits support that intention, or could they produce a different overall result?

- If gifting is part of the plan, is it genuinely affordable, properly recorded, and supported by evidence your executors can find later?

- Would a joined-up conversation between your Will planner and financial adviser improve the overall result?

If you are not sure, that is usually the signal to review the whole estate plan rather than tweak one document in isolation.

Cases

Comfortable, but closer than they think

Martin and Julie have a house, savings and investments worth about £900,000 between them, plus pensions they have mostly left untouched. For years, they assumed the pension side was separate. Once the numbers are reviewed properly, the question is no longer just what the Will says. It becomes what happens when the pensions are brought into the wider estate picture as well.

The unmarried couple with a false sense of safety

David and Anita are long-term partners, not married. Between them they have a house, investments and substantial pensions. They assume they are in roughly the same planning position as a married couple. They are not. Unmarried couples do not get the same spouse exemptions or transferable allowances, so pension wealth coming into the picture can make the exposure sharper and earlier.

The family at £1.8 million who still think they have time

Chris and Emma are sitting at about £1.8 million before taking pensions properly into account. They do not feel like a family who need serious inheritance-tax planning yet. But modest growth, combined with pensions, could move them through the £2 million line faster than expected. Their best move is not panic. It is a joined-up review while there is still room to plan calmly.

The widower with the large untouched pension

Alan is widowed, aged 78, with a valuable home, investments and a pension pot he has deliberately preserved because he wanted more to pass to the children. Under the current published position, that strategy may now create a different inheritance-tax outcome from the one he originally expected. It may also create an income-tax issue for the children depending on how the benefits are drawn.

The larger estate where charity is part of the plan

Margaret’s estate is around £2.6 million and she has always intended to leave money to charity as well as to her children. In her case, charity may support both her personal aims and the overall tax efficiency of the estate. But it still needs to be fitted into the wider Will and inheritance-tax plan properly.

Do pensions count for inheritance tax now?

Under current rules, many pension death benefits have often sat outside the estate for inheritance-tax purposes. The current published position is that this changes from 6 April 2027 for most unused pension funds and pension death benefits.

Will every family pay inheritance tax on pensions from April 2027?

No. Some estates will still remain below the relevant thresholds and some pension benefits may be treated differently. The point is that more families will need to review the numbers properly rather than assume pensions are irrelevant.

Can inherited pensions really face a 67% combined tax effect?

Yes, in a narrow worst-case illustration, but it is not a fixed tax rate. The 67% figure usually means 40% inheritance tax first, followed by 45% income tax on the remaining 60%. That leaves 33%. Whether anything like that applies depends on the estate, the pension, the age at death, the beneficiary, and the beneficiary’s own tax rate.

Can a trust solve this on its own?

Usually not on its own. A trust may still be very useful for control, protection and keeping inheritance on track, but pension exposure usually needs a broader joined-up review.

Can charitable giving help?

Yes, sometimes significantly. Gifts to qualifying charities are generally inheritance-tax free, and if at least 10% of the relevant net estate is left to charity, the inheritance-tax rate on the taxable part may reduce from 40% to 36%.

Does my Will decide who receives my pension?

Usually not. Pension death benefits are generally dealt with under the pension scheme’s rules. Most providers or trustees will consider the member’s nomination or expression of wishes, but they usually retain the final decision.

That is why the Will and pension nomination should be reviewed together rather than treated as separate documents.

Should I change my pension or my Will first?

Usually neither should be looked at in isolation. The better question is whether the overall estate plan, the pension nominations and the financial advice still line up.

This article is general information only, not individual advice.

If you would like help understanding the legal and estate-planning side, Fern Wills & LPAs can guide you through the options.

Where pensions are involved, we will usually recommend coordinated input from your financial adviser. If you do not have one, we can introduce you, with no obligation, to a financial adviser who understands the wider estate-planning picture.

Next steps

If pensions may now push your estate closer to inheritance-tax territory, this is the time to review the bigger picture.

Fern Wills & LPAs can help you work out whether the issue is mainly:

- a Will and estate-structure issue,

- a pension and financial-advice issue,

- or a joined-up planning issue needing both.

If appropriate, we can also introduce you, with no obligation, to a financial adviser who understands the wider estate-planning picture.

A short review now may prevent a much bigger tax or planning problem later.